Rescinded and Replaced by FIN-2020-R001

FIN-2008-R001

Issued: January 25, 2008

Subject:Reporting of Certain Currency Transactions for Sole Proprietorships and Legal Entities Operating Under a "Doing Business As" ("DBA") Name

The Financial Crimes Enforcement Network ("FinCEN") is issuing this administrative ruling to clarify the currency transaction report ("CTR") filing obligations when reporting transactions involving sole proprietorships. Subsequent to a prior ruling on this issue,1 FinCEN received feedback from financial institutions requesting further guidance. Therefore, in an effort to both enhance regulatory efficiency and provide complete and accurate CTR data to law enforcement, we are further clarifying the requirements of financial institutions reporting on currency transactions involving sole proprietorships and legal entities operating under a "doing business as" ("DBA") name.2 Because FIN-2006-R003 addressed a limited inquiry into the filing of CTRs on sole proprietorships, the present ruling is replacing FIN-2006-R003 and provides a more comprehensive discussion of the topic.

A sole proprietorship is a business in which one person, operating in his or her own personal capacity, owns all the assets and owes all the liabilities.3 Consistent with the definition of "person" in the Bank Secrecy Act’s implementing regulations,4 a sole proprietorship is not a separate legal person from its individual owner. Thus, when filing a CTR involving a sole proprietorship, financial institutions are required to complete one section ’A’, containing the name of the sole proprietorship’s owner5, the sole proprietorship’s DBA name, the owner’s social security number ("SSN"), home address, date of birth, and occupation.6 Only one section ’A’ is required, even if the business operations have a different address and/or tax identification number ("TIN") than its owner.7

However, to accommodate those financial institutions who wish to continue filing in accordance with FIN- 2006-R003,8 we will continue to accept CTRs completed with two section ’A’s when the transactions involve a sole proprietorship.9 FIN-2006-R003 stated that, when filing a CTR, financial institutions should provide information on both the sole proprietorship and its owner. Because the CTR form does not accommodate for both sets of information in a single section ’A’, FIN-2006-R003 stated that financial institutions should file two section ’A’s containing this information. An institution would check the "multiple persons" box, even though a sole proprietorship is not a separate person from its operator, to indicate that two section ’A’s were being completed.

The present ruling similarly applies to CTRs filed on legal entities operating under a DBA name. Whether the entity’s and DBA’s address and/or employer identification number ("EIN") are the same or different, when filing a CTR on a legal entity operating under a DBA name, financial institutions are required to complete one section ’A’ containing the name of the entity, the DBA name, the entity’s EIN, the entity’s address, and the entity’s business activity.10 However, to maintain consistency within the present ruling, we will accept two section ’A’s when filing a CTR on a legal entity operating under a DBA name.11

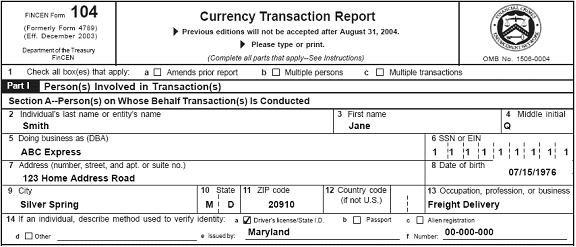

Example 1

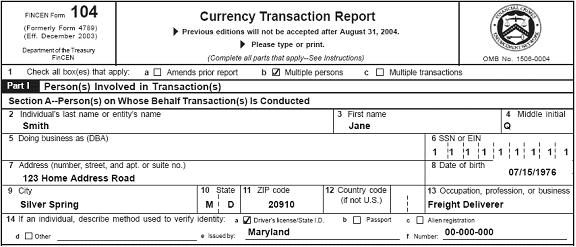

Jane Q. Smith operates a sole proprietorship that does business under the DBA name ABC Express. ABC Express does not have any employees, so Jane and the sole proprietorship have the same TIN. Jane lives at 123 Home Address Road and operates ABC Express from that location. Provided below is a proper way to file a CTR on a reportable transaction involving ABC Express.

Example 2

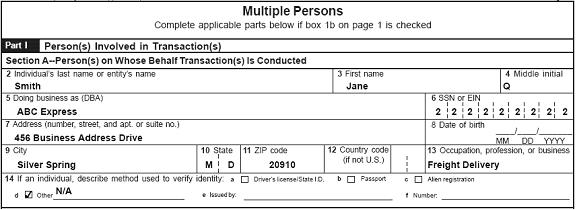

Jane Q. Smith operates a sole proprietorship that does business under the DBA name ABC Express. ABC Express has several employees, so Jane and the sole proprietorship have a different TIN. Jane’s SSN is 111-11-1111 and she lives at 123 Home Address Road. ABC Express’ EIN is 222-22-2222 and it is located at 456 Business Address Drive. Provided below is a proper way to file a CTR on a reportable transaction involving ABC Express.

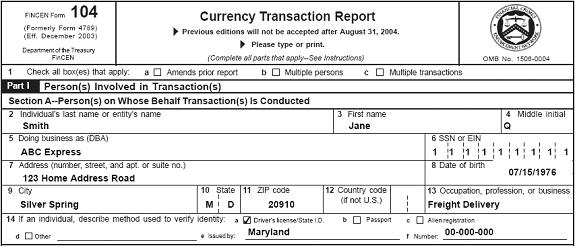

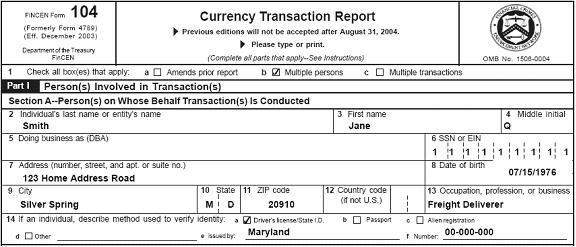

Example 3

Jane Q. Smith operates a sole proprietorship that does business under the DBA name ABC Express. ABC Express does not have any employees, so Jane and the sole proprietorship have the same TIN. Jane lives at 123 Home Address Road and operates ABC Express from that location. Provided below is a proper way to file a CTR on a reportable transaction involving ABC Express.

Page 1

Page 2

Example 4

Jane Q. Smith operates a sole proprietorship that does business under the DBA name ABC Express. ABC Express has several employees, so Jane and the sole proprietorship have a different TIN. Jane’s SSN is 111-11-1111 and she lives at 123 Home Address Road. ABC Express’ EIN is 222-22-2222 and it is located at 456 Business Address Drive. Provided below is a proper way to file a CTR on a reportable transaction involving ABC Express.

Page 1

Page 2

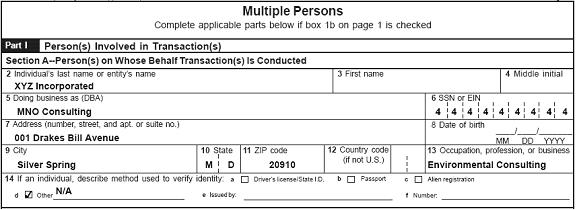

Example 5

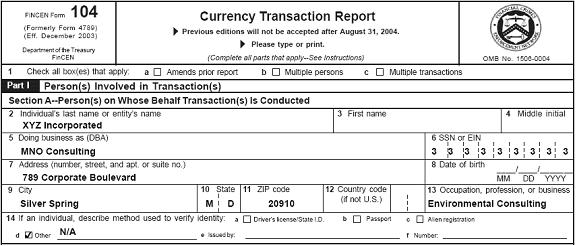

XYZ Incorporated, an environmental consulting corporation, operates under the DBA name MNO Consulting. XYZ Inc.’s EIN is 333-33-3333. XYZ Inc. registered MNO Consulting with its own EIN of 444-44-4444. XYZ Inc. is located at 789 Corporate Boulevard. MNO Consulting is operated at 001 Drakes Bill Avenue. Provided below is a proper way to file a CTR on a reportable transaction involving MNO Consulting.

Example 6

XYZ Incorporated, an environmental consulting corporation, operates under the DBA name MNO Consulting. XYZ Inc.’s EIN is 333-33-3333. XYZ Inc. registered MNO Consulting with its own EIN of 444-44-4444. XYZ Inc. is located at 789 Corporate Boulevard. MNO Consulting is operated at 001 Drakes Bill Avenue. Provided below is a proper way to file a CTR on a reportable transaction involving MNO Consulting.

Page 1

Page 2

1FIN-2006-R003 (Feb. 10, 2006) Currency Transaction Reports on Sole Proprietorships.

2See 31 C.F.R. § 103.86(a)(3).

3Black’s Law Dictionary 1398 (8th ed. 2004). This definition excludes a single member limited liability company ("LLC"), even one operating under the same tax identification number as its member, because the member operates the LLC in its capacity as a separate legal entity and the LLC, not the member, is responsible for its liabilities.

431 C.F.R. § 103.11(z).

5In states with community property laws that allow a husband and wife to operate an unincorporated business as a sole proprietorship, the sole proprietorship’s owner, for purposes of CTR reporting, will be the spouse whose social security number is attached to the sole proprietorship.

6See Example 1.

7See Example 2.

8For instance, an institution may wish to provide additional information for the benefit of law enforcement - as was the intention of FIN-2006-R003 - or because an institution’s computer systems may already generate CTRs in this manner.

9See Examples 3 and 4.

10See Example 5.

11See Example 6.