PDF Download : commercial_real_estate_assessment_final.pdf

An Assessment Based Upon Suspicious Activity Report Filing Analysis

December 2006

BACKGROUND

The Financial Crimes Enforcement Network (FinCEN) recently conducted a study of Suspicious Activity Reports (SARs) filed with FinCEN over a 10-year period that involved suspected money laundering and related illicit financial activity in the commercial real estate sector. This report focuses on certain trends in the reporting of suspicious activity in key businesses and professions in the commercial real estate sector. The report also provides summaries of SARs that were reviewed for this study as well as providing a range of examples of activities and transactions that may be indicative of money laundering and associated illicit financial activity.1

SIGNIFICANT FINDINGS

A random sampling of Suspicious Activity Reports describing commercial real estate transactions revealed that property management, real estate investment, realty, and real estate development companies were the most commonly reported entities associated with money laundering and related illicit activity. Professions that customarily collect fees in real estate transactions, such as appraisers, inspectors, surveyors, and attorneys, were reported as primary subjects with less frequency and, therefore, are not listed in the tables that follow.

Since 2003, the trend line in suspicious activity reporting associated with potential commercial real estate-related money laundering has risen steeply. The increase in filings has closely tracked similar trends seen in FinCEN’s recently issued mortgage loan fraud assessment. The increase is likely attributable to the steep decline in interest rate charges on real estate loans, which occurred contemporaneously with the increase in filings.2 It remains to be seen whether this trend in relevant suspicious activity reporting reverses as rates on real estate loans rise and the real estate markets cool.

METHODOLOGY

FinCEN used a Bank Secrecy Act (BSA) database analysis tool to obtain SARs of all types filed during the period January 1, 1996 through August 31, 2006, with narratives containing one or more key words generally associated with the commercial real estate sector.

Searches isolated 9,528 SARs that involved commercial real estate-related transactions or activities. Of these 9,528 SARs, 9,191 were filed by banks and other depository institutions, 271 were filed by securities and futures firms and 66 were filed by money services businesses. From this grouping, 960 SARs were randomly selected for review. The narratives identified 393 filings referencing commercial real estate-related transactions specifically.3

Using this same sample of SAR narratives (393 SARs), 260 (66.16%) identified transactions or activities that at a minimum involved suspected money laundering, structuring and related illicit financial activities. Of these 260 SAR narratives, 47 (18.08%) strongly suggested money laundering and related illicit activities. These 47 SAR narratives represented 11.96% of the total 393 narratives that referenced commercial real estate activities.

RESEARCH AND ANALYSIS

The 260 SAR narratives reviewed were found to fall into five categories: structuring, money laundering, international transfers, tax evasion, and miscellaneous illicit activity.

Structuring Activities Related to Commercial Real Estate

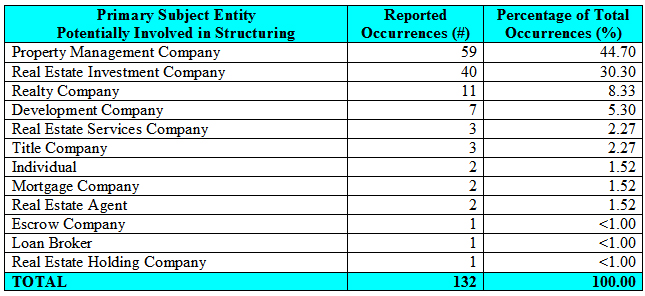

Of the 260 SAR narratives studied in depth, the largest set of filings (132) reported suspected structuring of deposits and/or withdrawals 4. Table 1 shows a breakdown (in descending order of incidence) of the sampled SARs describing commercial real estate-related businesses, professions and individuals potentially involved in suspected structuring.

TABLE 1

It will sometimes prove difficult to determine when subjects structure particular commercial real estate-related business transactions to promote money laundering. Nevertheless, the following examples illustrate suspected structuring that likely was conducted with the intent to launder funds.

1. A U.S. bank reported that on one day an individual used cash to purchase three cashier’s checks, each for an amount at or near $10,000 at three different locations of the same bank, and payable to the same payee, which was a title company.

2. A U.S. bank reported that during a nine-day period, an associate of a bank customer reportedly made structured cash deposits into the bank customer’s account from an unknown source. The bank customer, who owned rental properties, also reportedly wrote four checks each in face amounts at or near $10,000, payable to one individual, within a five-week period, which began sixteen days before the first structured cash deposit and ended ten days after the last cash deposit was received in her account. The relevant circumstances included structured cash deposits from an unknown source, followed by checks written in amounts facilitating structured negotiation. In addition, the aggregate amount paid out in checks was five percent less than the aggregate amount deposited in cash.

Money Laundering Activities Related to Commercial Real Estate

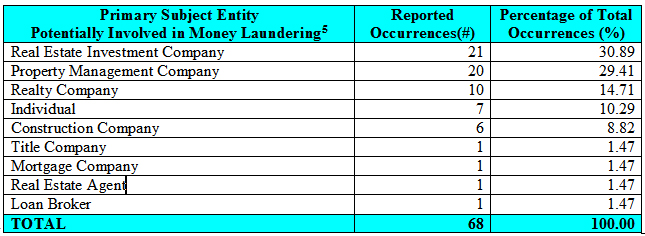

Sixty-three of the 260 SAR narratives described activities deemed suspicious and are generally indicative of money laundering. Table 2 shows a breakdown of the SARs describing businesses, professions and persons potentially involved in activities generally indicative of money laundering.

TABLE 2

The following examples illustrate suspicious commercial real estate transactions or activities likely conducted to facilitate money laundering.

1. A U.S. bank reported that funds were being transferred between several real estate- related accounts in a circular fashion for no apparent legitimate reason. The accounts were linked by common account signers. Several businesses were involved, and they were all located at the same address and had the same account signers. Various news articles indicated that these companies had been involved in alleged real estate fraud.

2. A U.S. bank reported that a real estate investment company located in the eastern part of the United States made multiple cash deposits within a five-week period in amounts that totaled almost one million dollars. During this same period, the company sent wire transfers to and received wires from a single company located in the western part of the United States. In total, the wires involved amounts that approximated the cash deposits.

3. A U.S. bank reported that over a two-week period, a real estate investment company used cash to purchase numerous cashier’s checks. Most of the checks were purchased for amounts just under the $3,000 recordation threshold 6. These checks were deposited to an account in the name of the check payee at the filing bank. A review of bank records showed that this account also received deposits composed primarily of numerous cashier’s checks sold by another bank (most issued in amounts near the recordation threshold). Bank employees reported that at different times an account signer would identify himself by presenting driver’s licenses from different states bearing significantly different names, and signatures executed in significantly different handwriting styles.

4. A U.S. bank reported that the principal of a real estate investment company deposited a substantial amount of funds in traveler’s checks to his business account. He refused to identify the source of these checks when asked by the bank.

5. A U.S. bank reported that principals of a real estate investment company frequently withdrew large amounts of cash, purchased monetary instruments, and re-deposited many of the monetary instruments back into the real estate investment account. These activities occurred over a three-year period and involved amounts that totaled in the millions of dollars. The filer believed this activity was inconsistent with the normal operation of a real estate investment company.

6. A U.S. bank reported that the principal of a real estate investment company deposited over $100,000 in cash into the company’s account. When asked for the source of the funds, the individual stated that she had saved the money from an unrelated business. Much of the currency was in small denominations.

7. A U.S. bank reported that an individual transferred money from his line of credit account, through his personal account, through his property management account, and back to his line of credit account for no apparent personal or business reason.

International Transfers Related to Commercial Real Estate

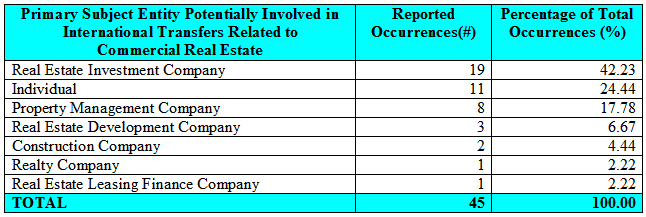

Out of the 260 SAR filings, 45 described international movement of money related to commercial real estate. Table 3 shows a breakdown of the SARs describing businesses, professions and persons potentially involved in international transfers of funds to facilitate money laundering or other related illicit financial activity.

TABLE 3

The following examples were deemed suspicious by filers and illustrate how commercial real estate transactions or activities involving international transfers of funds likely were conducted in order to facilitate money laundering and other related illicit financial activity.

Money Laundering

1. A U.S. bank reported that one of its business customers, a company registered on a Caribbean island and allegedly involved in real estate sales, was associated with a crime family in a foreign jurisdiction. As such, the bank suspected that the company was used to facilitate the family’s illegal business operations. When the bank proposed terminating its relationship with the customer, bank employees working in the crime family’s home country warned bank personnel that a closure of this account could physically endanger bank personnel working in the crime family’s home country.

2. A U.S. bank reported that a group of its customers involved in property management admitted to sending large wire transfers to a European country so that the money could be wired from there to Iran. The customers claimed they were sending the money to finance construction in that country. The bank determined that these activities violated the Iranian transactions regulations issued by the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) and terminated the account relationship.

3. A U.S. bank reported that one of its account holders, who claimed to own many properties in a Latin American country, was depositing numerous money orders allegedly representing rental payments, into his personal account and sending many wires to the country in which he owned the properties, purportedly to pay employees there. The filer believed that large numbers of money orders deposited to a personal account followed by large transfers through Latin American transfer companies appeared suspicious.

4. A U.S. bank reported it received a large wire transfer on behalf of a company registered in the Caribbean, which purportedly developed commercial and residential real estate projects in a Latin American country. The account holder claimed these funds represented a legal settlement with a governmental agency in the Latin American country. The bank transferred the funds to an account in Europe at the account holder’s request. It was subsequently learned from news reports that the account holder had been accused of fraud by a Latin American governmental agency.

5. A U.S. bank reported that its customer, a purported part-owner of a Latin American company engaged in real estate investments, received three wires sent from his company to his personal account. The wires involved amounts that totaled in the hundreds of thousands of dollars. The customer sent personal checks to various Latin American exchange houses. The filer suggested this activity could be a money laundering scheme.

6. A U.S. bank reported that a Latin American business, which purportedly provides property management and representation services for an American business operating in a Latin American country, was also a money exchanger / money transfer company and travel agency. Deposits into the company’s bank account included numerous checks payable to multiple payees in amounts that totaled in the millions of dollars.

7. A U.S. bank reported that a real estate lease financing company received numerous even multi-thousand dollar checks from individuals and businesses across the country for deposit. Subsequently, the bank paid even multi-thousand dollar checks issued by the company to various individuals who all negotiated the checks in a specific Middle Eastern country.

8. A U.S. bank reported that an account holder traveling in Iran attempted to transfer money from Iran to the United States, purportedly for the rental or purchase of commercial property. The bank official involved in the transaction became suspicious since the account holder claimed to be an international lawyer and was unfamiliar with OFAC regulations.

9. A U.S. bank reported that two non-resident aliens, who were purportedly real estate investors, made structured cash withdrawals from their account following receipt of wire transfers. The funds were presumably from an oil company located in their home country.

10. A U.S. bank reported that an individual associated with various real estate-related companies wired nearly a million dollars to himself through various accounts in the United States and a nearby country. The filer concluded the individual appeared to be engaged in layering activities.

11. A U.S. bank reported that a property management company received sequences of money orders for deposit. The company also issued numerous checks, in the $3,000 to $9,000 range to a single individual, which were cashed out over a year-long period. According to the filer, the principal of the company made large loans to others, which were often quickly repaid. The principal maintained a joint personal checking account with a relative, who has since left for the Middle East. The principal made cash deposits below the currency transaction reporting threshold and subsequently sent wire transfers to one account in a Middle Eastern country.

Politically Exposed Persons 7

1. A U.S. bank reported that one of its account holders approached the bank to apply for a substantial loan to purchase a business. The account holder received wires totaling in the hundreds of thousands of dollars from his country of origin. According to bank records, this individual had a low income. Nonetheless, he claimed to have been a government official in his native country.

2. A U.S. bank reported that an individual associated with real estate investments in the United States had sent and received millions of dollars in transfers to/from countries in Asia. The bank’s research concluded the individual may have laundered money for politically exposed persons in a particular Asian country.

Potential Tax Evasion Activities Related to Commercial Real Estate

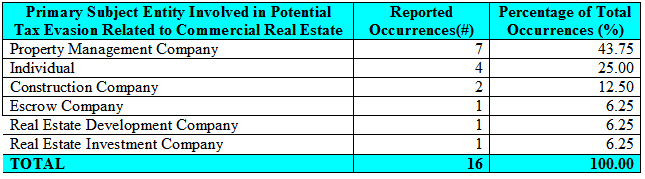

Table 4 shows a breakdown of the sampled SARs describing commercial real estate-related businesses, professions and persons involved in alleged activities generally indicative of tax evasion.

TABLE 4

The following examples were deemed suspicious by filers and illustrate commercial real estate transactions or activities likely conducted to facilitate tax evasion.

1. A U.S. bank reported that the principal of a property management company purchased numerous cashier’s checks each in amounts at or near $10,000 and payable to himself from funds in one of his corporate accounts. The principal then cashed the checks over a period of time.

2. A U.S. money services business reported that multiple money orders, all in small denominations, were purchased at various locations and made payable to a property management company. One group of money orders was purchased in aggregate for more than $3,000, the recordation threshold. An unknown individual endorsed all of the money orders and deposited the instruments in a bank account.

3. A U.S. bank reported a similar scenario in which checks payable to multiple property management companies controlled by the same principal were periodically cashed out rather than deposited to bank accounts.

4. A U.S. bank reported that the principal of a real estate investment company inquired about setting up his business accounts so that the Internal Revenue Service (IRS) could not place levies on the accounts.

5. A U.S. bank reported that a construction company appeared to be exchanging its company checks for cashier’s checks purchased from a check casher.

6. A U.S. bank reported that a commercial real estate developer issued checks to a rental property owner in denominations each under $10,000.

7. A U.S. bank reported that the principal of a property management company, who was in the business of administering Section Eight low-income housing, deposited checks to his property management account lacking transfer endorsements and made payable to a different property management company. The principal was determined to be associated with a signer on the account of the other property management company, held at the filing bank. The filer suggested these activities may have represented a tax evasion scheme.

8. A U.S. bank reported that a construction company paid other companies for goods and services with sequences of checks, each under $10,000.

9. A U.S. bank reported that the owner of a discount store who also rented commercial properties had changed the deposit pattern into her business account. Whereas previously the account received deposits of commercial checks from various businesses indicating “rent” on the checks’ memo lines, the account stopped receiving these deposits and began receiving cash deposits.

10. A U.S. bank was used as an intermediary for payments from the owner of a company located in Latin America to an individual in a European country for the purchase of undeveloped land in that country. An amount approximating $100,000 was transferred from the Latin American business to the account of a customer of the U.S. bank. The money was then transferred to the country in Europe in subsequent wires each sent on a monthly basis for the purchase of the land. When questioned as to why the Latin American company did not simply send a wire transfer directly to the bank of the land seller in the European country, the account holder admitted that the purchaser was attempting to hide the source of funds and the seller wished to evade taxes in the European country where the land was located. The bank concluded that it was used as a “layering bank.”

11. A U.S. bank reported that an individual with a commercial real estate line of credit entered the bank to make a payment on his loan. The individual had a bag of cash in his possession and asked the teller to count out enough money to make his payment and pay something against the principal, but to not exceed $10,000, because he wanted to avoid detection by the IRS.

12. A U.S. bank reported a novel scheme concerning real estate investment and a Roth Individual Retirement Account (IRA). A bank customer reportedly devised a strategy by which he could make real estate investments through his Roth IRA. Profits from the real estate investments were credited back to the Roth IRA, which then invested the funds in various companies including the account holder’s businesses. The account holder’s personal contributions to the Roth IRA were minimal, but with the real estate profits deferred from taxes in the Roth IRA, the account’s value had ballooned to millions of dollars.

13. A U.S. bank reported receipt of seven wire transfers from the IRS within a one-week period for credit to the same bank account. The wires purportedly represented tax refunds associated with the purchase of real estate. The bank quickly ascertained that these refunds were based on false tax documents filed with the IRS, and returned the money to the IRS. The bank concluded that the refunds were associated with a scam in which investors in the real estate were supposed to reap a substantial return on investments within a short period of time.

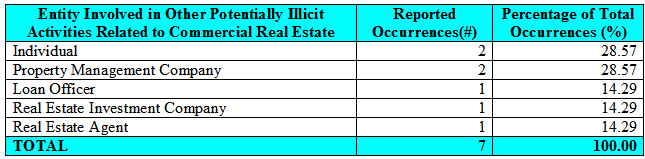

Money Laundering to Promote Other Commercial Real Estate-Related Potentially Illicit Activities

Table 5 shows a breakdown of the sampled SARs describing commercial real estate-related businesses, professions and persons involved in a range of other potentially illicit activities.

TABLE 5

The following examples were deemed suspicious by filers and illustrate suspected money laundering activities used to facilitate other potentially illicit activities tied to the commercial real estate sector.

1. A U.S. bank reported that it had discovered a relationship between a relative of one of its senior executives and a realtor who was conducting transactions for a politically exposed person. The relative reportedly received a large check from the realtor, which she deposited into a certificate of deposit and a Roth IRA. The money belonged to the politically exposed person. Bank investigators secured documentation bearing the name of the realtor from the office of the bank official involved in the investigation. The bank official indicated that the politically exposed person had loaned the money to the realtor for investment. The bank officer said he believed the realtor gave the money to the bank officer’s relative to avoid taxes and for safekeeping.

2. A U.S. bank reported that many of the loans in the portfolio of a former bank loan officer were past due. Many of the payments that were being made were made by individuals other than those obligated on the loans. Many of these loan payments were also reportedly made in cash or by cashiers check purchased with cash. Several of the subject loans involved the purchase of commercial real estate.

3. A U.S. bank reported that an account holder who is the signer on an apparent real estate investment account is also an employee of a large American city. This individual deposited large sequentially numbered money orders with face amounts at or near $10,000 into this company’s account. Some of this money could be linked back to the city’s Section Eight housing funds for low-income people. The narrative also indicated that other city employees also had real estate-related business accounts that appeared to be linked to these activities.

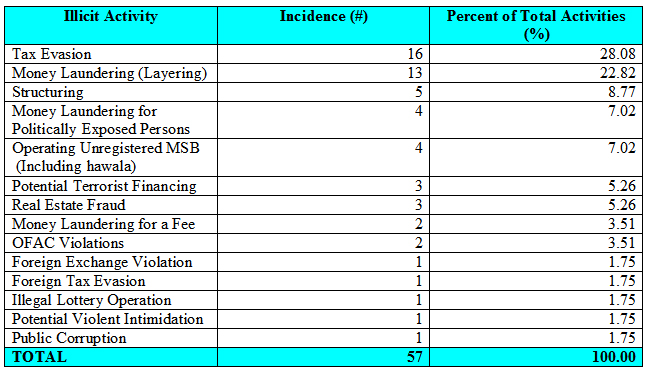

Characterizations of Suspicious Activity

A total of 47 of the 260 sampled SAR narratives reported activities strongly suggesting money laundering. Table 6 shows the various illicit activities reported or suggested in these 47 narratives in decreasing order of incidence.8

TABLE 6

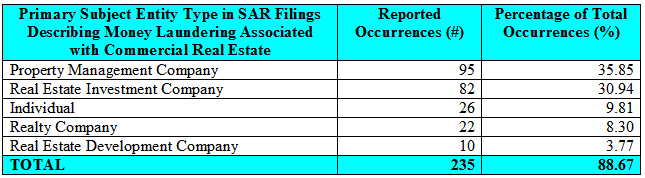

Top Businesses, Professions, and Persons

Table 7 shows a breakdown of the SARs describing the top five businesses, professions, and persons involved in activities generally suggesting money laundering, structuring, and related illicit financial activity.

TABLE 7

SAR narratives indicated that the greatest amount (78.86%) of structuring, money laundering and associated illicit activity tied to the commercial real estate sector occurred through property management, real estate investment, realty, and real estate development companies.

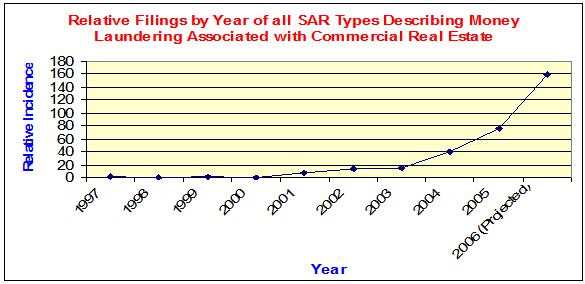

Filing Trends

Graph 1 aggregates all types of SAR filings reporting possible structuring, money laundering and associated illicit activity tied to the commercial real estate sector. It shows steep increases in the relative numbers of filings after 2003. This study used a random sample of the whole data set. Numbers on the y-axis represent numbers associated with the sample.9

GRAPH 1

SUMMARY

In the SARs reviewed for this study, the most commonly reported suspected illicit financial activity associated with the commercial real estate sector is money laundering to promote tax evasion. The SARs revealed illicit activity committed or attempted by principals of all types of businesses associated with commercial real estate, especially the principals of property management companies, real estate investment companies, and construction companies. The SARs indicated that the individuals engaging in such schemes often attempted to cash out checks payable to their businesses, pay cash for construction materials, and trade negotiable instruments with other business people to understate business receipts and actual business volumes as a way to avoid audit trails and evade taxes. The SARs showed an increase in the reporting of transactions using real estate-related accounts to launder money for politically exposed persons and for facilitating informal value transfer systems.

The SARs also identified an increase in the reporting of commercial real estate transactions used to facilitate money laundering and associated criminal activities. The trend appeared to rise significantly in the 2003-2004 period, which mirrors most activity patterns seen in the mortgage loan fraud assessment. This increase in reporting occurred during the expansion of the real estate market brought on by lower real estate lending rates.

This study may have been limited by the difficulty many financial institutions have identifying money laundering in the integration stage of a scheme. Notwithstanding the recent trend in property flipping addressed in the mortgage loan fraud assessment, real estate has historically been a relatively illiquid asset. Under normal market conditions, it generally takes several months to sell residential or commercial properties. Consequently, these conditions generally have not favored the money launderer seeking to layer his funds quickly, moving them from one account or investment to another. It is probable that real estate has been most useful to money launderers in the integration stage where it may serve as both an investment and vehicle to store the value of laundered funds.

1Money laundering is the disguising of funds derived from illicit activity so that the funds may be used without detection of the illegal activity that produced them. Money laundering involves three stages: placement, layering, and integration. Placement involves placing illegally obtained funds into the financial system. "Dirty" money is most vulnerable to detection and seizure during placement. Layering means separating the illegally obtained funds from its source through a series of financial transactions that makes it difficult to trace the origin. During the layering phase of money laundering, criminals often take advantage of legitimate financial mechanisms in attempts to hide the source of the funds. Integration means converting the illicit funds into a seemingly legitimate form. Integration may include the purchase of businesses, automobiles, real estate and other assets.

2See FinCEN publication Mortgage Loan Fraud: An Industry Assessment Based Upon Suspicious Activity Report Analysis at /system/files/shared/MortgageLoanFraud.pdf.

3This number (393 SAR narratives) represents 40.94% of the total sample size. When scaled against the total number of SAR filings identified that reference commercial real estate search terms, this predicts about 3,900 SARs in the database that substantively reference commercial real estate transactions.

4Structuring occurs when a person, for the purpose of evading reporting or recordkeeping requirements under the Bank Secrecy Act, causes or attempts to cause a financial institution to fail to file reports or make records; causes or attempts to cause a financial institution to file reports or make records that contain material omissions or misstatements of fact; conducts or attempts to conduct one or more transactions, in any amount, at one or more financial institutions, on one or more days, in any manner, including the “breaking up” of a single sum that exceeds a reporting or recordkeeping threshold into smaller sums at or below the threshold. See 31 U.S.C. 5324; 31 C.F.R. 103.119gg); 31 C.F.R. 103.63. Although structuring is frequently associated with money laundering and is often an indicator of it, the reasons for structuring financial transactions vary.

5In several instances, more than one individual or entity was involved in the suspected money laundering activities.

6The Bank Secrecy Act requires financial institutions to record information relating to the purchase of certain monetary instruments in amounts that equal or exceed $3,000. See 31 C.F.R. 103.29.

7According to the Federal Financial Institutions Examination Council’s Bank Secrecy Act/Anti-Money Laundering Examination Manual , a politically exposed person is a person identified during account opening or maintenance as a “senior foreign political figure,” any member of a senior foreign political figure’s “immediate family,” and any “close associate” of a senior foreign political figure.

8Several narratives reported multiple activities. Provided narratives often contain references to specific suspicious characterizations in whole, in part, or in combination with another activity or activities. The filer may have reason to believe indicators exist relative to multiple activities, which may or may not be related to one another.

9The last data point on the graph was projected based on the number of SARs filed through August 31, 2006. The trend in Graph 1 corresponds closely to the trends seen throughout the mortgage loan fraud assessment. Numbers remain relatively stable in the 2001-2003 period and then spike after 2003.